A Journey From Barter to Bits | Course Episode #1

The Origins of Money & Blockchain + The Crypto Opportunity

A Journey From Barter to Bits | Course Episode #1

Hello My Friend,

Welcome to the first episode of our 12-Part Course ‘A Journey From Barter to Bits’ where we are going to dive into the origins of money, the invention of blockchain and discuss the opportunity that lies ahead for this innovative technology.

I’ve built this session with one objective in mind; to help you understand that money evolves.

In fact, it’s the how and why money has evolved over the course of human history that has brought you to this course today as you’re curious on how cryptocurrencies (or what many call, magical unicorn money) can play an integral part in our human economy in the 21st century.

We’re just about ready to dive in but before we do;

😌 Please make sure you’re comfortable & relaxed, we have about 10-15 minutes of reading ahead.

🎙 Take note of the option to hear this episode as a podcast episode, located in the podcast section of our substack.

📖 Lastly, take a look top-down at our learning points for today’s session.

A Journey From Barter to Bits | Course Episode #1

Let’s start our journey by traveling back 10,000 years when Hunter Gatherers roamed the earth.

You see, hunter gatherers had no money per se.

Rather, each band member hunted and gathered natural resources to make almost everything they required - they were generally unaware that life existed outside of their bands.

Individuals within the band each had a role;

One would hunt for meat.

One would make those animal hides into clothing.

Perhaps another would use the bones, rocks and sticks to make weapons.

Meanwhile another would use special plants to make medicine.

We can see that band members may have specialized in different tasks, but they shared their goods and services through an economy of favors and obligations.

This basic economy was a direct trade of resources without any form of hard 'money' - simply a barter for goods that each member lacked.

Common items bartered were food, tools & weapons.

Over the course of thousands of years humans evolved from foragers to farmers.

The Agricultural Revolution, also known as the Neolithic Revolution began around 10,000 BC and continued through to 1,400 BC.

As the earth entered a warming trend, humans began planting and growing their own crops as the traditional nomadic lifestyle transitioned to more permanent agricultural settlements.

Life itself became more sedentary and the populations in these settlements began to grow in size.

As a byproduct, a larger variety of finished goods such as shoes, tools & herbal medicines became a focal point of skilled villagers to produce as the earliest stages of commerce and trade was awakened.

The economy was shifting from an economy of favors and obligations, where the ledger of transactions remained solely in the conscious minds of humans, to a new economy of goods and services which would require a much more efficient database.

The earliest accounting dilemma would now surface as our ancestors struggled to measure the intrinsic value that each finished good would be ‘worth’ and how to transact and transport these goods safely and easily.

They would invent a system of measurement that would become the yardstick of intrinsic value.

The invention of money.

Cowry shells were amongst the earliest documented forms of money.

The shells became an intrinsic value measurement system (also referred to as 'currency') due to their durability, convenience, divisibility, as well as being easily identifiable - all important aspects of a currency.

💡 It’s worth noting that historians have speculated that simultaneously across various regions of the globe, alternative forms of currencies may have included animal hides, salts & spices as well as hand-made weapons.

These shells were used in Asia, Africa and parts of Europe and were accepted as the first symbol of wealth and power.

A predetermined quantity of shells were able to represent a specific good or service thus allowing for each item to have a specific value.

For example 1 bag of cowries may have contained 20,000 cowrie shells.

Human “A” could purchase a pair of wooden shoes for 1000 cowries.

If Human “B” wished to purchase a large amount of food it may have cost 10 bags of cowrie shells.

Humans were on the verge of establishing the first measurement scale of intrinsic value, or medium of exchange relating to resource sharing.

Bartering is only effective with a limited range of products, however not optimized for a complex economy with products & services.

Cowry shells would be the first solution to quantifying needs & wants with a tangible currency.

As villages and communities grew in size with an array of goods to be shared, trade routes were cemented.

With the passage of time, the interconnectedness of these geographically populated areas would take a new form, Kingdoms.

Kingdoms and smaller cities brought the rise of improved infrastructure & transport which allowed for new opportunities for human labor specialization.

Densely populated cities provided full-time ‘employment’ for the producers of goods & services, and no longer would a human life require waking hours to be dedicated purely to survival of the fittest.

💡 The human brain is an incredible innovation of nature. The brain itself contains mirror neurons which has allowed humans to learn and adapt to changing environments. As civilization matured, humans were blessed with the privilege of being born into a community with endless time to be educated and master new skills including language, sciences & trades.

Niche villages would gain a reputation for producing the highest quality oils, other areas the finest of wines, meanwhile others specialized in clothing and or medicines.

While Cowry shells were a fantastic monetary system where the shells were scarce and populations smaller, as trade routes grew geographically the shell system was rendered ineffective with new trading partners across Asia and India.

Cowry shells in these areas could be easily sourced naturally and counterfeited, meaning there was no longer trust in the system and no longer value in these types of shells for trade.

During the early middle ages some of the earliest forms of process technologies were being discovered by man-kind.

Humans have long used their primal instincts to extract solutions from nature - and the science of metallurgy was a solution that would transcend civilization.

With the rise of Kingdoms and Empires, leaders of these territories began using the newly discovered science of Metallurgy to 'mint' coins using precious metals such as bronze and eventually gold.

These new coins were a paradigm shift that restored the trust to their money system which allowed trade to further flourish across multiple Kingdoms & Empires.

Minted coins were superior in durability and could be marked with an imprint of significance by each leader, King or Emperor.

The mark on each coin assured trust and insured convertibility amongst merchants and trading partners.

For 750 years minted coins comprised the majority of trade settlements until coinage encountered a problem of its own; clipping.

Clipping involved shaving small shards from metallic coins to produce a homemade hammered version of the accepted legal tender of the age.

Again, we see the issue of trust & counterfeiting creating the need for a system upgrade.

The monetary system would not only require a unique marked stamp atop the coin guaranteeing its acceptance, but also the base metal to be increasingly rare.

Silver & Gold would become the de-facto base metals of choice.

In fact, the first coin minted in gold called the Florin became the most widely accepted currency across Europe which encouraged the beginnings of international trade & the very beginnings of a colonial wealth hierarchy.

Marco Polo, a Venetian merchant, explorer and writer who traveled through Asia along the Silk Road between 1271-1295 had visited China and discovered that the Emperor of China had a monetary policy very different from the coins in Europe - a system of paper note currency backed by coin reserves.

The trust of this system was authorized by a Chinese inscription that warned "those who are counterfeiting will be decapitated" - a very serious threat declared by the emperor state.

Marco Polo discovered that merchants in China could store their metal coins with a trusted depository for a verified paper note so that they didn't have to transport their heavy coins on far travels.

💡 As we progress through our travels in time, it’s important we begin to identify repeating cycles and patterns throughout money’s evolution. We have so far learned that the foundation of money requires collective trust, and without it a new system must be designed.

And we’re about to identify a new property of money; one to which a keen metaphor may be suitable.

Much like the movement of water, a liquid, can be described as a current, the swift movement of money, or liquidity, can be described as ‘current-cy’.

After returning from his travels, Macro Polo introduced this concept to Europe and paper money experimentation began its adoption curve for international trade.

These paper notes could be taken to a bank of coins at any time and exchanged for their face value in metal, usually silver or gold coins.

This paper money could be used to buy goods and services. In this way, it operated much like currency does today in the modern world.

(And we will soon learn that currencies prefer speed over stalemate.)

Thousands of years have passed since hunter-gathers intuitively bartered with one another for the resources they required.

The agricultural revolution blessed humans with the privilege to settle and enabled densely populated areas to transform into Kingdoms.

Kingdoms & Empires allowed for human intellect to flourish and international trade routes connected mankind using currencies as the handshake of trust.

Merchants from across the globe had the ability to travel East to West carrying paper notes signed by their respective Kings, Emperors or leaders of any kind to foreign lands to transact and gather goods such as tea, raw materials and luxuries of the day.

The next obstacle of money we faced as humans became the redemption of these various currencies issued for the correct or fair amount of minted coin equivalent.

Would a paper note from a small island nation be trusted the same as a paper note from an Austrian monarchy?

What was preventing the mass printing or excess supply of paper notes from an underdeveloped nation with no coinage depositories from traveling East or West and falsely claiming their currency could be trusted for redemption?

The solution was a gold redemption standard monetary system where a standard paper note is based on a fixed quantity of gold.

A trade agreement was drafted and each participating country's currency in paper money became equivalent to a specific amount of Gold to be redeemed.

International monetary exchange could now be issued between countries on this new gold exchange standard which guaranteed a fixed exchange rate.

This meant that one countries currency could be traded for another countries currency using the gold standard exchange rate.

Gold would become the standard metal to reflect all hard money.

The gold standard was the basis for the international monetary system from the 1870’s to the early 1930’s and again from 1944 to 1971.

🛑 Let’s make a quick pitstop on theory to address a common pattern.

For thousands of years we have experienced the cycles of monetary systems and the respective technologies that humans have used to facilitate a global system of exchange and trade - it appears the innovation cycles are getting shorter as humans get smarter;

ATM Cards & Point of Sale Systems allowed for withdrawal of paper money from the bank with ease and convenience, this established trust that people could store their money safely within an institution and they could return anytime and withdraw it from their accounts to spend their money.

ATM cards were now debit cards and could be used for a variety of purchases and were debited electronically from their bank accounts, this encouraged a flourishing economy & more spending with ease.

The innovation of smartphones and high speed internet allowed for the introduction of mobile and internet banking.

The Credit System, specifically Visa & Mastercard consumer credit cards as well as bank loans for mortgages allowed humans for the first time to borrow on the promise of future repayment with interest, or profit paid to the lender for the issuance of funds today.

Interest rates and access to credit were based on a human score compiled by a blend of meritocratic & proprietarian factors.

✅ We will keep these points in mind as we move forward.

What have we learned so far about money?

Money is NOT shells, coins or banknotes.

Money IS anything that people are willing to use in order to systematically represent the value for the purpose of exchanging goods and services.

The purpose of money is to enable humans to quickly and easily compare the value of different commodities for exchange or storage of wealth, thus money must have two primary features: convertibility & trust.

What we have learned so far is that money is a system of mutual, collective trust - and not just any system of trust; money is the most universal and most efficient system of mutual trust ever devised.

But what happens when this trust is broken on a considerably larger scale?

Let’s continue.

Faced with mounting inflation and debt from World War II, the Nixon administration decided in August 1971 to end the convertibility of U.S Dollars into Gold.

With the collapse of the gold standard agreement (known as the Bretton Woods Agreement) in the early 1970s, the United States struck a deal with Middle Eastern nations to standardize Oil prices in dollar terms and provided U.S. financial markets with a source of liquidity and foreign capital inflows and elevated the U.S. dollar to the World's reserve currency.

💡At the time, the world was progressing through the Industrial Revolution, where Oil was the most in-demand commodity of the time as it fuelled the production manufacturing machines of each nation in addition to human mobilization via car, truck, plane and train.

With this agreement, the USA had complete control of the global monetary system and their banks utilized fractionalized banking regulations (where the trusted depositories could lend out multiples of currency relative to their backing deposits) to stimulate their local economy while immensely growing their profits.

Additionally, The Federal Reserve, the primary issuer of the U.S Dollar now controlled the nation's interest rates to speed up or slow down the U.S economy, also known as monetary policy.

The global money system has now reached its peak of centralization, owned and controlled by the world’s most dominant economy, the United States.

If the ‘Fed’ lowered interest rates, this would allow corporations to obtain credit and create jobs at the expense of a controlled inflation.

Alternatively, when the Fed raised interest rates this would slow inflation but also increase unemployment.

As more money was added to the system, also known as quantitative easing, the inflation rate of the monetary supply increased and the ‘dollar’ would become less valuable in terms of purchasing power as more debt was incurred to maintain the nation.

The U.S enjoyed 50 years of pristine growth at the expense of foreign nation labor and exports, but this could only last so long.

As history has proven over and over with the cycle of money, the system of trust would be broken - in epic proportion.

💡In hindsight it’s transparent that all of history’s most prominent financial meltdowns; for instance The Great Depression of the 1920’s & Dot-Com boom in the early 2000’s, were for the most part due to over-leveraging the amount of currency supply (like dollars) relative to hard money (like gold) depositories on hand.

When financial actors lend out money they do not own and get caught, big problems ensue.

The 2008 Financial Crisis was born of irresponsible (or greedy) lending by the world's largest banks, selling a product known as subprime mortgages (risky low interest rate housing) to unqualified consumers.

These lending products were very profitable for banks and they issued them without fear largely due to the fractionalized banking regulations that they pushed too far.

In 2008 these debt obligations reached a peak and the consumers that had borrowed owed far more than they could repay, leading to a cascade of defaults that nearly brought the global financial system to its knees.

💡 It’s important to remember that the money being lended to unqualified consumers for profit were the deposits of other citizens who believed their money to be safe and guaranteed for redemption at any time.

As an emergency solution, the Federal Reserve printed relief funds that injected capital into the troubled banks & institutions to prevent a global financial system collapse.

Can you identify the big obstacle repeating in our monetary system at first glance?

There was a broken line of trust on a global scale that began the downfall of the currency system of international trade.

The financial near-collapse of global markets exposed that the banks and the institutions responsible for holding human capital (money and currency) were giving out large amounts of client funds that risked the security of those funds for profit.

We would need a system upgrade to rebuild global trust.

As history repeats, when a money system is broken humans look to the technologies of the times for a solution:

A Database Problem: The favors and obligations economy looked to nature for a solution; cowry shells.

A Trust Problem: The early middle ages looked to the newly discovered science of metallurgy for a solution; minted coins.

A Trust Problem: The counterfeiting of minted coins led to seeking a more trusted rare metal base; gold.

A Speed Problem: When gold became too slow to transport, paper money was the solution.

A Convertibility Problem: When Paper Money became difficult to redeem, an exchange rate was born.

As we can see, the money system continually evolves to be more trusted through collective agreements on the convertibility of currency to hard money, as well as increase the speed of the currency transactions to improve liquidity in global trade.

Let’s return to our most exciting part of today’s episode, the birth of Bitcoin.

Circa August - October 2008 an unprecedented series of events occurred somewhat simultaneously;

The U.S Government established a $700 Billion Troubled Assets Relief Fund to prevent a global financial system collapse.

Bitcoin.org was registered and a Whitepaper publication was uploaded, authored by an unknown entity named Satoshi Nakamoto.

One could theorize that the concept of Bitcoin rose like a phoenix from the ashes of a Wall St. induced monetary system failure.

The published paper detailing the technology behind the Bitcoin network of trust founded the basis of what would be known as blockchain technology and the first Bitcoin block of transactions was created containing 50 bitcoins - a brand new modern day currency.

The unknown creator ‘Satoshi’ made clear he was attuned to the failings of the global financial system as on the genesis block of Bitcoin's Blockchain he left a lesson for the world to learn from.

💡 The identity of Satoshi is highly debated and speculated to this day whether the name represents an individual, a group of individuals or perhaps a group of nation representatives.

This anonymity would make sense to ensure global collective trust rather than credit the invention to a single origin.

Satoshi left a message on the network's first block of transactions by inscribing: "The Times 03/Jan/2009 Chancellor of the brink of second bailout of banks."

Blockchain promises to restore the ‘trust’ to how humans transact in a modern day economy due to its decentralized nature, removing cycles of human greed from the equation.

You may be asking, how does Blockchain differ from Cryptocurrencies?

Blockchain is to Cryptocurrencies what iPhone is to Apps, a platform technology comprised of hardware components & software code.

Blockchain is the underlying layer to which cryptocurrencies may be built atop.

As a technology, it is considered to be one of the greatest inventions of our digital age as we are at the precipice of a global monetary system turnover.

Blockchain has the potential to revolutionize the way governments, institutions and modern day societies conduct business and financial transactions, as for the first time in history humans have created a trust-less third-party system to record & exchange data.

So, how does Blockchain work? Remember that we understand money has two primary features, convertibility and trust - thus blockchain must have benefits to help enhance these required traits - and it does so spectacularly.

In summary, and let’s say this together:

“Blockchain is a digital ledger that publicly records all transactions in a sequential, secure, permanent and ever-expanding chain of cryptographic hash-linked blocks."

Let’s break this definition down to our caveman friends from 10,000 years ago.

Immutable Digital & Distributed Ledger: Solving The Database Problem

A digital file that publicly records all transaction history from all users visible to everyone restoring the trust factor that is essential for money.

Distributed ledgers use independent computers which are referred to as nodes to record, share and synchronize transactions in their respective electronic ledgers - instead of keeping data centralized as in a traditional ledger.

Immutable Ledger is a record that cannot be changed. In the digital age we need data security and proof that the data has not been altered - that's the only way we can trust the digital data.

Cryptographic Security: Leveraging Modern Day Computer Technology

Cryptography is the study of secure communications techniques that allow only the sender and intended recipient of a message to view its contents. Here, data is encrypted using a secret key, and then both the encoded message and secret key are sent to the recipient for decryption.

The encoding uses a highly sophisticated mathematical problem solving method to hide secure and lock information.

Sequential Transactions: Improving Speed of Accounting

Transactions recorded in chronological order.

An ever-expanding connected chain of transactions that continues to grow & expand.

Hash-Linked block of files linked to each other by highly advanced algorithms.

Proof-of-Work Consensus: Solving the Trust Layer of Money

The proof of work (PoW) was the original consensus algorithm used by Bitcoin to approve transactions.

It requires the many network participating accountants (computers) to collectively agree that their respective versions of the Bitcoin ledger are all the same before adding new transactions to the network, guaranteeing no counterfeiting of the currency or database.

Rather than a Federal Reserve, King or Emperor stamping coins or printing dollar bills, each cryptocurrency network may have a predetermined supply of currency built into its code.

As transactions are performed on a blockchain network, also referred to as a distributed ledger network, computers race to solve the cryptographic puzzle of each block and add the transaction to their respective versions of the ledger and submit their hard work to the network for approval.

When the cryptographic puzzles are solved that becomes the "proof" and the cryptocurrency transaction is now created & recorded on the blockchain.

This method was originally referred to as ‘mining’ on the Bitcoin network.

With a Proof of Work Consensus (POW), the original ‘network approval’ mechanism built by Satoshi, the first miner to solve the puzzle gets rewarded in fractions of the cryptocurrency transaction, which is how the currency would be issued over time.

💡Satoshi engineered Bitcoin to have a max supply of only 21 million Bitcoins ever produced. This ensured that the network would eventually have no inflationary concern. The network is predicted to have issued all coins by the year 2140.

It’s worth noting that since Bitcoin’s inception in 2008, developers have taken distributed ledger technology to new heights by taking Bitcoins’s original concept and improving on the code for added features and benefits to the network.

As you can imagine, as the value of Bitcoin's network rose, the reward received by miners became a very lucrative endeavor.

This would lead to corporations building farms of highly sophisticated computers requiring incredible amounts of energy to enter the Proof of Work race.

Developers of blockchain technology forecasted that this would be a problem long term and began editing the ‘consensus algorithm’ of new networks to become more environmentally friendly.

The edits of the original Bitcoin code spawned an industry of innovation like no other.

While Bitcoin was the Father of Cryptocurrencies, the evolution of blockchain technology has spawned variations to the features and benefits of the original code, with the offspring networks dubbed altcoins.

Early modifications of the open-source code of Bitcoin lead to coins such as Ethereum, Ripple, Litecoin & Dogecoin, popular crypto’s with the global community.

As of 2022 over 20,000+ cryptocurrencies exist and are in circulation with each network aiming to solve a modern day problem facing humanity.

While Bitcoin may have been conceptualized to focus on a payments and hard money problem, new networks are aiming to solve problems in real estate, insurance, derivatives markets and tokenized assets.

The list is growing by the day of how blockchain can be used to create a network of trusted value.

The current market cap of crypto globally is over $1 trillion dollars.

Our World is becoming increasingly digital - much like the internet did decades ago, cryptocurrencies are radically transforming legacy financial and information systems.

To become an investor in digital assets and cryptocurrencies is to believe that the future of humanity is approaching faster than we think.

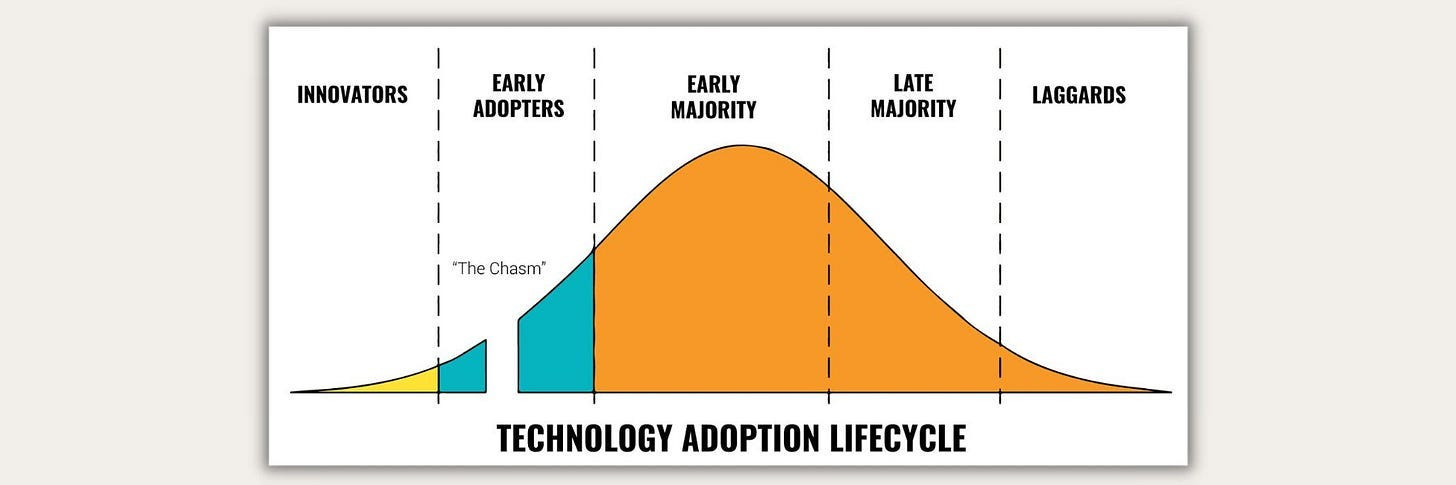

The Innovation Adoption Curve below classifies the entry of users into various categories, based on their willingness to accept a new technology or an idea.

It is useful in breaking down or segregating consumers into five different segments or categories such as innovators, early adopters, early majority, late majority, and laggards - as you can see, we are early.

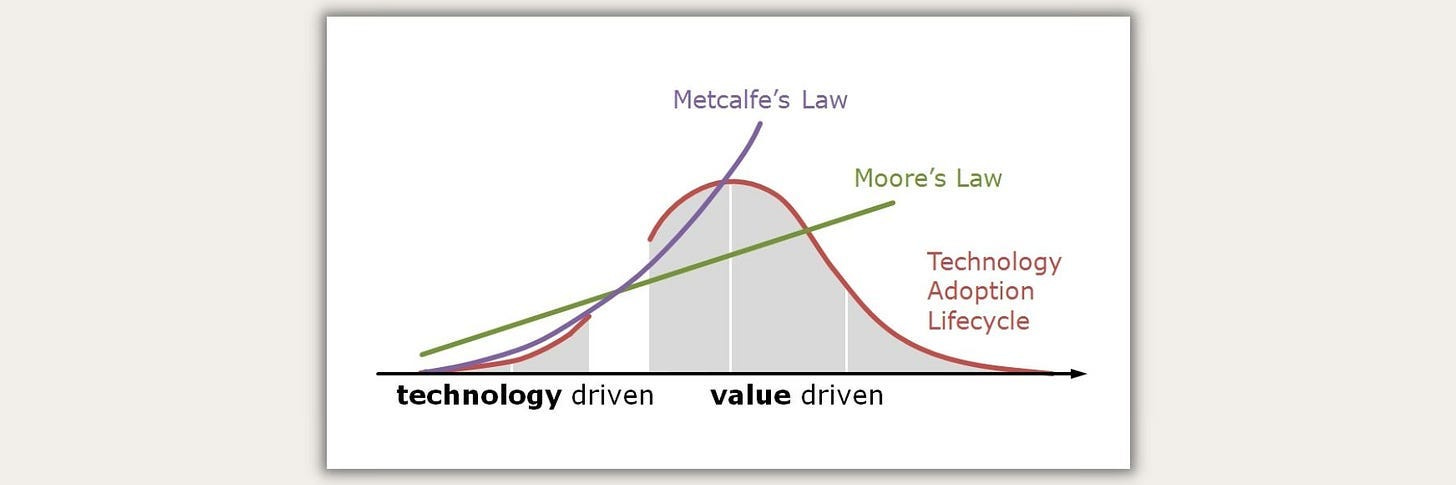

Metcalfe's Law says that a network's value is proportional to the square of the number of nodes in the network - this is directly analogous to the 'trust' aspect law of money.

Moore's Law states that we can expect the speed and capability of our computers to increase every couple of years, and we will pay less for them - this is directly analogous to an exponential value-driven curve.

Digital currencies are at the center of several trends reshaping the global investment landscape by evolving the free market paradigm and placing pressure on the leaders of our world to restructure their ideologies of banking and transnational financial regulations & monetary policies.

What was once land & buildings, machinery, precious metals & stocks being sought after as the most lucrative capital assets of the global economy is now transforming into a decentralized digital ecosystem built upon blockchain technology.

The evolution of money has spanned thousands of years as human civilization matures, we just happened to be alive at a special time to witness one of these monumental moments unfold.

You may also enjoy:

Course Episode #2 | Learning the Basics of Crypto Security, Digital Wallets & Navigating Exchanges

Course Episode #3 | Learning the Basics of Technical Analysis

👋🏼 Hey!

Thanks for reading today’s newsletter.

If you have any comments, feedback or questions on any material written in this edition please share as I'd love to continue a dialogue below.

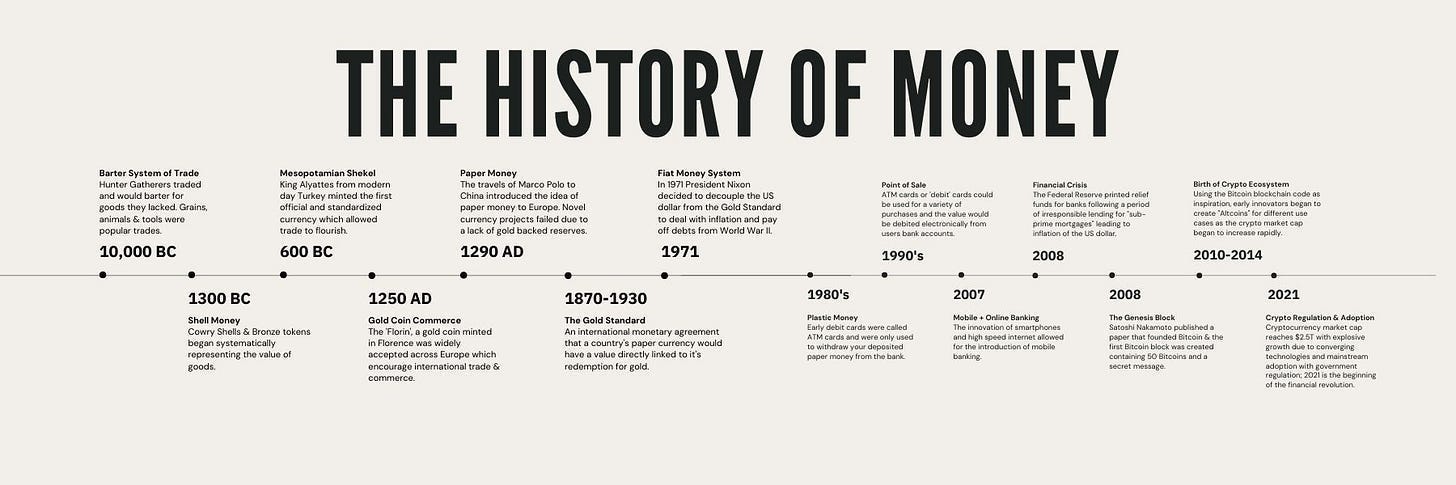

Appendix: The History Of Money Timeline